The interest rate on fixed deposits, whether provided by a financial institution, a government enterprise, or a private corporation, is calculated in two ways. The first is simple interest, and the second is compound interest.

Both types of interest are calculated only on the principal investment, but they differ in their consideration of the principal amount. This leads to a difference in the amount of return received by the investor at the end of their investment tenure.

Keep reading to understand the critical differences between these two types of interest calculations.

Simple interest is calculated using the formula SI = P × R × T/100 , where:

P is the principal amount

R is the annual interest rate

T is the time period

Compound interest is calculated using the formula CI = P× (1 + R/n) ^ n×T − P, where:

P is the principal amount

R is the annual interest rate

n is the number of times interest is compounded per year

T is the time period

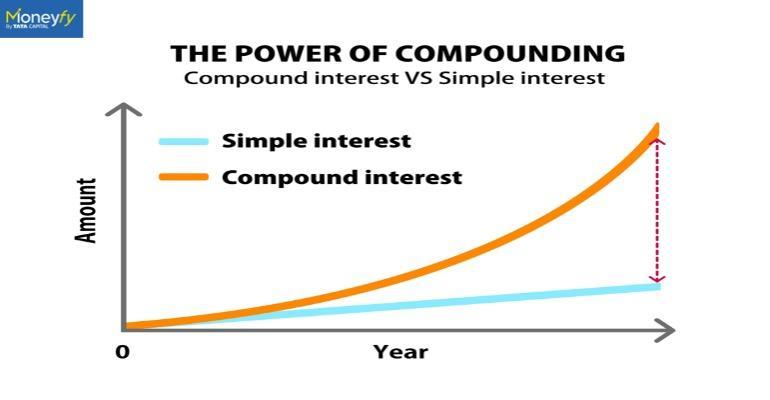

In the long run, compound interest returns are typically higher than simple interest returns due to the former’s exponential growth. The key difference between the two lies in the calculation method. The calculation of simple interest is based on the original principal, whereas the calculation of compound interest is based on both the principal and accumulated interest.

Here’s a table summarizing the difference between simple and compound interest.

| Aspect | Simple interest | Compound interest |

| Growth pattern | Linear | Exponential |

| Basis of calculation | Constant throughout the investment or loan tenure | Alters with every compounding period |

| Interest on interest | No | Yes |

| Potential returns | Comparatively lower | Has a higher potential, especially over long periods |

| Common uses | Certain fixed-income investments, short-term loans | Savings accounts, long-term investments, and credit card balances |

| Impact of compounding frequency | None | Higher compounding frequency results in faster growth |

Suppose you invest Rs. 10,000 at a 5% annual interest rate for 3 years. Using the simple interest formula, the total amount after three years will be:

SI = P x R x T/100

SI = 10,000 x 5 x 3/100 = Rs. 1,500

Now, consider the same Rs. 10,000 investment at a 5% annual interest rate, but this time compounded annually for 3 years. Here, interest is calculated on the principal plus any accumulated interest. Using the compound interest formula, the interest earned after 3 years will be:

CI = P x (1 + R/n) ^ n x T − P

CI = 10,000 × (1 + 5%)^3 - 10,000 = Rs. 1,576.25

Interest, simple and compound, has the following effects on the way your money accumulates.

To calculate compound interest, use the formula CI = P× (1 + R/n) ^ n×T − P, where:

P is the principal amount

R is the annual interest

n is the number of times interest is compounded per year

T is the time period

The primary difference between simple and compound interest is how interest is calculated. Simple interest is calculated only on the principal amount throughout the investment period. In contrast, compound interest is calculated on the principal as well as on the interest earned.

SI is computed solely on the initial principal whereas CI is calculated on the principal and any accumulated interest, resulting in substantial growth.

There is no difference between SI and CI for one year when the principal and rate of interest are the same. This is because, in the first year, compounding hasn’t taken effect yet. So, both SI and CI give the same interest amount.

This depends on whether you're investing or borrowing. If you're investing, compound interest is better because it helps your money grow quickly by earning interest on both the original amount and the interest earned. But if you're borrowing, simple interest is better because you only pay interest on the original loan amount.

Some financial products that use simple interest include bank deposit accounts, credit cards, certain lines of credit, etc.

The interest compounding period can vary. It can be either daily, monthly, quarterly, or annually.

Yes, compound interest on investments, such as bonds or savings accounts, is considered income under the head for ‘Income from Other Sources.’

Click the “Allow” button to receive notifications

We're constantly crafting offers and deals for you. Get delivered straight to your device through website notifications.

All you have to do is click on “Allow”.

Now keep a track on your favourite fund

Go to the watchlist page to remove a fund from the list.

No funds are added to watchlist

Add your favourate funds to watchlist to keep them handy

Funds Added to Compare 00/03 00/02

No funds are added to portfolio

Add your favourate funds to portfolio to keep them handy

Funds Added to Compare 00/03 00/02

Trust the links that start from https://www.tatacapitalmoneyfy.com

Do not make payments

in any individual’s bank accounts.

Reach our Customer Care moneyfycare@tatacapital.com for assistance

For any assistance, contact our customer support

4 mins read

4 mins read